The Ban of MasterCard

Introduction

It was a major move when RBI banned Mastercard from issuing new cards due to non-adherence to domestic data storage regulations on the 14th of July, 2021. In India, one out of every three card transactions is processed through the Mastercard Network. Before getting into the details of the ban, let's explore the scenario and structure of card payments in India.

Scenario of Card Payments in India

Debit and Credit Cards were introduced in India in the early 90s. Initially, it took time for people to shift to card payments but as the trust was built, the cards network grew eventually. However, the catalyst which kickstarted the growth cycle of card payments were the steps taken by the Modi Government such as Demonetization and Digital India.

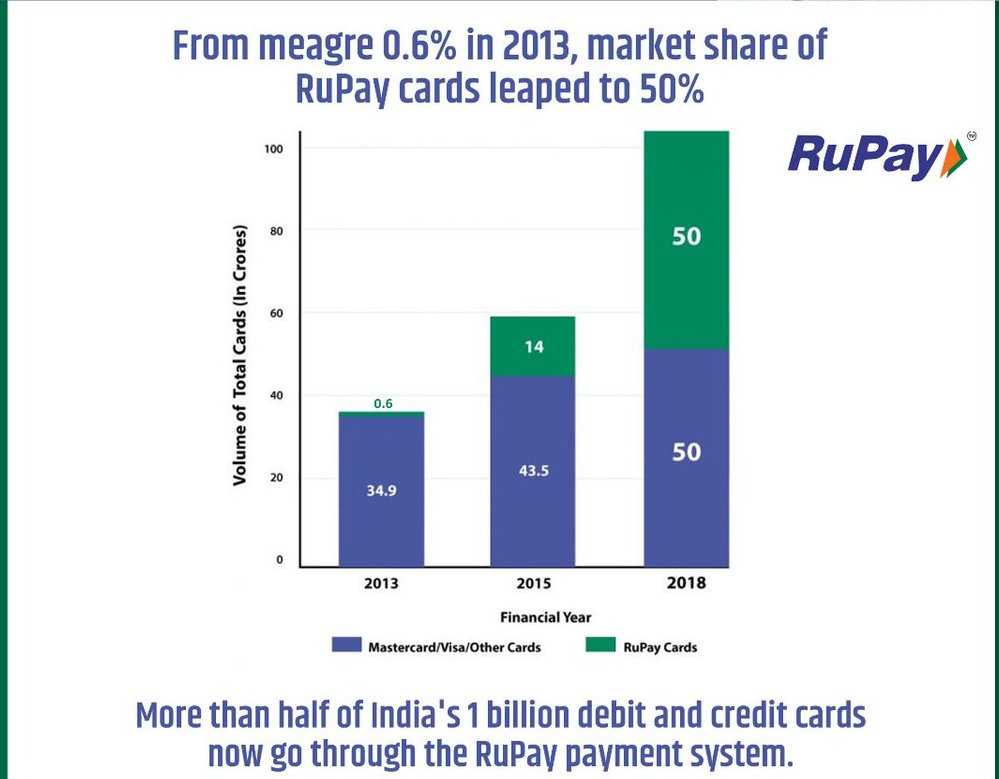

In India, a majority of the banks have been providing four networks through which Debit and Credit Card payments are made: Visa, Mastercard, Maestro (a part of the Mastercard enterprise) and RuPay. RuPay is the only one of the above which is Indian and it was launched in 2012. Earlier, the sector was completely dominated by the foreign players.

The Modi Government has been promoting the use of national networks since 2014. In 2014, it introduced the financial inclusion campaign of Jan Dhan Yojana wherein the people of the country (especially from Tier-3 and Tier-4 cities) were offered zero balance bank accounts at nationalised banks along with a RuPay Debit Card. They did not consider any foreign card networks. Then in 2018, Modi urged the people to use national cards instead of the foreign ones. On seeing all this, Mastercard raised this issue with The Office of the US Trade Representatives and claimed that the government was promoting the use of RuPay with nationalism. However, Mastercard didn’t lag behind and announced a whopping $1 Billion investment in 2019 over a period of five years in India to upkeep its customer base. Thus, the ban comes as a major loss for the American Network.

Why was Mastercard banned?

The Reserve Bank of India (RBI) on 14th July, 2021 indefinitely barred Mastercard Inc from issuing new debit, credit or prepaid cards to domestic customers for violating data storage rules, dealing a blow to the US company in a key market. The ban takes effect on July 22. This comes after RBI banned AMEX and Diners Club in May this year citing the same reasons.

In a notification, the RBI said Mastercard had not complied with data storage rules from 2018 that require foreign card networks to store Indian payments data only in India so the regulator can have "unfettered supervisory access".

The RBI said that the restrictions have been imposed, as in spite of a lapse of considerable time and adequate opportunities being given, the entity has been found to be non-compliant with the directions on storage of Payment System Data.

How will it impact existing customers?

The Government did clarify that the existing Mastercard customers will not be affected by this directive and steps are being taken to safeguard the data of the citizens of the country. All card-issuing banks and non-banks will be advised to follow these guidelines by Mastercard. Mastercard will no longer be able to issue new cards after July 22. However, it will be able to serve its existing customers.

How did Mastercard React?

Mastercard said it was disappointed with the RBI's decision and that it had provided regular updates on its compliance with the rules since 2018.

“Building on our considerable and continued investments in India, we remain committed to working with our customers and partners in advancing on the government’s Digital India vision,” Mastercard said.

Impacts

According to Nomura Research, RBL Bank, YES Bank, and Bajaj Finserv are the ones most impacted by the ban as all their credit card schemes are allied to Mastercard. Among others, IndusInd Bank, Axis Bank, and ICICI Bank have 35-40 per cent of their credit card schemes tied to Mastercard, the report said. Though HDFC Bank has 45 per cent of its credit card schemes tied to Mastercard, since it is already restricted from issuing new cards, the lender is not incrementally impacted.

RBL Bank has entered into an agreement with Visa Worldwide to start the issuance of credit cards on the Visa platform, the lender informed the indices. The bank issues 1,00,000 new credit cards per month and this will potentially remain impacted until either the ban on Mastercard is lifted or their technical integration with Visa is complete, which is expected to take 8 to 10 weeks.

Who can benefit the most?

Customers of American Express and Diners Club had flocked to RuPay, which is owned by RBI’s National Payments Corporation of India, and was already a dominant player with a market share of around 60%(In terms of issuance of new cards) in November 2020. Experts believe a similar trend will follow Mastercard’s ban. Mastercard currently accounts for nearly 33% of all card payments in India. But RuPay having zero Merchant Discount Rate and not having international acceptance might lead to an increase in Visa’s market share.

With Mastercard getting banned, major channels will be Visa and RuPay. Most of the banks will be partnering with more than one payment company now, and many PSU banks are already offering RuPay cards.

The other beneficiary of the ban could be the Unified Payment Interface (UPI), a partly state-owned digital payment system. UPI payments, which are done from one bank account to another without adding a beneficiary, can be a replacement for debit cards. The UPI payment process is easier, faster, and more secure, which makes it a contender to replace card payments. In addition, there are no transaction charges on UPI payments, unlike credit cards.

What follows the ban?

With American Express already banned, the Mastercard ban will surely increase the burden on the banks to establish a new structure for issuing new cards through Visa and Rupay Networks. This delay in transition to other networks will affect the bank fees and other incomes they generate from the card business for the next few months. In a research note on RBI's decision, Macquarie flagged as a "key concern" the risk that banks could suffer as credit cards were a profitable product with a so-called post-tax return on assets of around 5% to 6%. However, looking at the positive side, RBI believes that if the data needs to be secured then we must restrict the breaches.

That’s all for this week! We hope you liked it and would love to know your thoughts in the comment section. This article is written and curated by Vaibhav Agarwal and Shivang Goenka.

(Vaibhav Agarwal is a 2nd year student pursuing BCom(H) at St. Xavier’s College (Autonomous), Kolkata and a Junior Associate of the Xavier’s Finance Community.)

(Shivang Goenka is a 2nd year student pursuing BCom(H) at St. Xavier’s College (Autonomous), Kolkata and a Junior Associate of the Xavier’s Finance Community.)